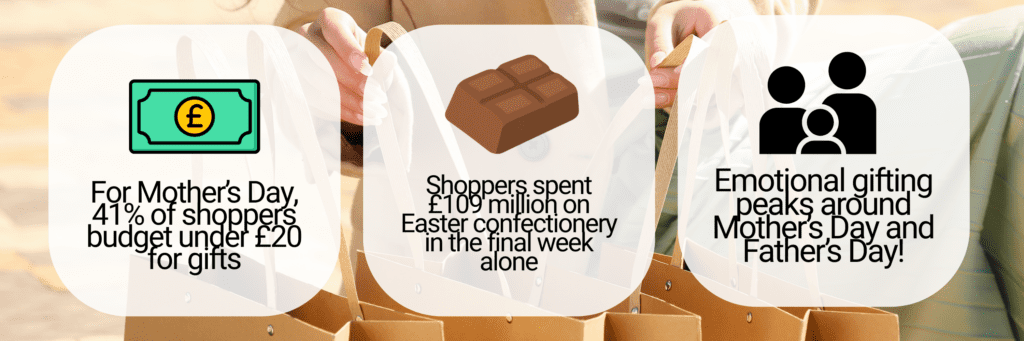

Q2 doesn’t usually get the fanfare of Q4, yet it consistently delivers some of the most meaningful and emotionally charged retail moments of the year. From Easter through to Father’s Day, this period brings a blend of gifting, seasonal resets, and renewed consumer optimism. But in 2026, that optimism is fragile - shaped by economic uncertainty, heightened price sensitivity, geopolitical matters, and a retail landscape that demands continuous operational excellence to compete. For retailers and brands, Q2 represents both a challenge and an opportunity. And for those supported by an end‑to‑end retail partner, the opportunity is even greater. The Q2 Consumer: Selective, Cautious, Intent-Led Thanks to the lack of promotional frenzy that is commonly experienced in Q4, Q2 shoppers buy more intentionally.Seasonal occasions such as Mother’s Day continue to drive participation. Last year, spending for Mother's Day 2025 hit an estimated £1,673 million, up 5.3% year-on-year. Despite this, spending remains deliberate, with 41% of shoppers budgeting under £20 for gifts. This reflects a broader shift toward selective purchasing and value-led decision making. Emotional gifting peaks around Mother’s Day and Father’s Day, where shoppers prioritise meaningful products and personalisation. Barclays consumer spend data highlights this tension clearly: while 46% of consumers say they are cutting back on non-essential spending, one in five (20%) are still willing to prioritise spending on memorable occasions and celebrations. This dynamic played out over the Mother’s Day weekend, which delivered a notable retail uplift. High street retail transactions rose 40.1% versus the 2025 daily average, restaurants saw transactions increase 37.9%, and florists experienced a 553% surge in purchases on the Friday before Mother’s Day. Seasonally, Easter and spring trigger a broader wave of “reset behaviour.” Many consumers use this period to refresh their homes, wardrobes and social routines as the weather improves. Kantar data shows strong seasonal demand in categories such as outdoor living (+24%) and gardening (+51%), while broader retail sales typically strengthen in spring as consumers prepare homes and lifestyles for the warmer months. Easter alone generated £9.2 billion in UK grocery sales, up 4.9% year-on-year, demonstrating the continued scale of seasonal spending moments. However, this growth was largely price-led, with volumes increasing by just 1.3%, showing that shoppers are spending more per item but purchasing more selectively. Despite this caution, the desire to celebrate remains strong. Shoppers spent £109 million on Easter confectionery in the final week alone, while promotions accounted for nearly 30% of grocery spending during the Easter period, as retailers worked to maintain value perceptions. Kantar notes that retailers who captured the most Easter share were those that activated earlier in the season and aligned promotions and product mix with evolving shopper behaviour. Yet despite these clear demand signals, many brands still treat Q2 as a transition period between peak retail seasons. The result is often late campaign activations, fragmented stock availability, weak product bundling and generic gifting messaging, leaving retailers under-leveraged during a period when consumers are actively looking to refresh all areas of their lives. The Economic Underpinning: Why Q2 2026 Feels Different Economic reality will shape consumer behaviour in Q2 more than in previous years. Our Retail Economic Outlook March 2026 (Acosta Europe) provides essential context: This combination of weak consumer confidence, elevated cost pressures, and persistent price sensitivity means brands face a Q2 where intention to purchase exists, but barriers to conversion are higher than ever. Retail & Brand Pain Points in Q2 2026: 1. Under‑forecasting Demand in Short Planning Cycles Q2 events like Easter, Mother’s Day, Father’s Day have short lead times and peak on specific dates. Consumers shop last‑minute, expecting fast, frictionless fulfilment and strong availability. Brands frequently under-forecast demand and activate campaigns too late, a costly mistake. CommerceIQ data reinforces this, showing inventory instability and out‑of‑stock–related revenue losses rising 3.8% YoY. [commerceiq.ai] 2. Intensifying Price Sensitivity & Own-Label Appeal Rising food inflation, especially in seasonal categories like chocolate and confectionery for Easter, is reshaping spending. Consumers are trading down or switching to private-label alternatives. Last year, Chocolate confectionery prices rose 17.4%, the fastest in any category, yet volume still grew 0.4%, indicating shoppers were willing to pay more for seasonal products despite cost pressures. Despite this, Kantar reports premium own‑label growth of ~23.2% in recent weeks around Easter as shoppers balanced value and quality, a powerful proof point for private label appeal in Q2. Implication for Q2: Easter confectionery, Mother's Day giftables, and spring home/lifestyle products are highly sensitive to price and promotions — brands must balance value perception with premium appeal. 3. Rising Costs & Margin Pressure Global disruptions continue to impact margins, particularly transport, logistics, energy, and commodity costs, which are amplified in Q2 by seasonal spikes in product demand (e.g., chocolate, flowers, fresh produce). Implication for Q2: Seasonal peaks intensify margin pressure — especially when consumers expect value promotions without sacrificing availability. 4. Fragmented Inventory & Weak Omnichannel Execution Q2 campaigns often suffer from stock fragmentation and inconsistent bundling, particularly for gift packs, Easter baskets, and themed seasonal products. Implication for Q2: Brands that fail to unify online and in-store availability risk losing out on peak-season purchases, when consumers are actively seeking convenience and curated offers. Q2 Themes Retailers Must Lean Into 1. Value Reset Consumers define value differently, sometimes through price, sometimes through quality, convenience, or emotional resonance. Q2’s emotional gifting moments demand thoughtful, frictionless, and personalised solutions. 2. Convenience as a Dealbreaker Shoppers default to convenience when timelines are short. Speed, clarity, and visibility matter more than promotions. 3. Inspiration Over Discounting Spring resets are driven by newness and curation, not blanket promotions. 4. Digital Shelf Battles Intensify Brands with consistent availability and accurate on-shelf placement outperform peers, with out-of-stock situations directly contributing to a 3.8% YoY revenue loss. Success in Q2 depends on ensuring the right products are in the right place at the right time, with clear pricing, robust stock levels, and strategic merchandising. During Q2 seasonal peaks like Easter, Mother’s Day, and Father’s Day, fulfilment reliability, both in-store and online, is critical, as consumers increasingly expect fast, frictionless access to seasonal favourites. Brands that combine robust inventory, clear merchandising, and dependable delivery capture more sales, even under short planning cycles and high price sensitivity. How we can help you solve Q2’s Challenges: Field Marketing & Rapid Activation This ensures brands don’t miss short Q2 windows and drive visibility exactly when intent peaks. Product & Supply Chain These capabilities offset economic pressures like rising fuel costs and imported goods inflation. Ecommerce & Digital Shelf Excellence Essential when digital-first shoppers trade down, compare constantly, and demand convenience. E-Fulfilment & Last‑Mile Operations Critical in a Q2 environment where shortened planning windows can make or break revenue. Q2 May Be Quieter, but It’s Where Growth Is Won Q2 2026 presents a unique blend of: For brands and retailers, this is not a period to under-resource, it’s a period to execute with precision. With the right end-to-end retail partner, Q2 becomes a growth accelerator, not a missed opportunity. By combining rapid field activation, seamless omnichannel execution, robust supply capabilities, and intelligent fulfilment, retailers and brands can not only navigate uncertainty, they can outperform it. Get in touch today to see how we can help you.